Against a background of rising costs and unaffordable car insurance, provincial government interventions in Alberta’s auto insurance market have increased markedly over the past decade. Several different types of reform have been implemented in an attempt to address rising premiums. The government has tried increasing the authority of the Automobile Insurance Rate Board (2014), limiting awards for pain and suffering (2020), and introducing direct compensation for property damage (2022), among others. One “solution” they have chosen to use repeatedly is price controls (i.e., rate caps).

Price controls have proven highly detrimental to Alberta’s auto insurance market, sending strong anti-free-market signals to both consumers and insurers. Over time, such interventions undermine the very functioning of the market itself. To restore stability and efficiency, the government should refrain from interfering and allow premiums to be determined by competition and market forces.

Multiple Forms of Meddling with Insurance Prices

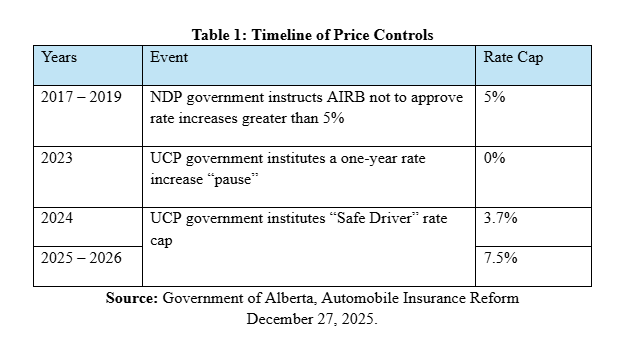

Historically, various Alberta governments have implemented price controls on auto insurance. For example, between 2017 and 2019 the NDP government imposed a cap of 5% on all rate increases across the board. By 2019, this rate cap had become unsustainable and the incoming UCP government removed it. Within 18 months the auto insurance regulator of Alberta, the Automobile Insurance Rate Board (AIRB), approved significant rate increases for 95% of the province’s auto insurers. Four years later, however, in 2023, that same UCP government introduced an even more restrictive price control than the NDP had: a year-long “pause” on all rate increases.

When the pause ended in January 2024, it was replaced with a “safe driver” rate cap, set at 3.7% for eligible drivers. A “safe driver” was defined by the government as someone who had had no at-fault accidents in the past six years and no major or minor convictions in the past three years. At the time, the government estimated that 80% of drivers would be eligible for this status. In 2025, the government allowed the “safe driver” rate cap to increase to 7.5%, and has decided to keep this in place for 2026.

The Pernicious Effects of Rate Caps

Price controls have been tried by governments throughout the ages and across the globe, and they have invariably led to perverse effects. When maintained despite these effects, they eventually cause the destruction of the underlying market itself.

When prices are prevented from adjusting freely—as in the case of imposing rate caps on auto insurance—the result is price distortions, shortages, misallocation of resources, and quality deterioration. As these results intensify, motorists and insurers adapt their behaviour. For example, motorists have less incentive to avoid risk, and more incentive to pursue claims they might otherwise have paid out-of-pocket. Insurers become more selective about whom they insure, run stricter claim investigations, and less insurance options. They may even stop offering auto insurance and leave the market entirely. As these behavioural changes develop, the government often imposes additional regulations and controls.

In insurance markets, such distortions are especially devastating, because insurance is fundamentally about pricing risk. Constraining premiums prevents accurate risk pricing and leads to lower profitability or even outright losses. For example, an increase in the number and gravity of accidents, and of damage and reparations claims, will drive the cost of covering insurance claims above revenues (in the form of premiums collected). Insurers are thus forced to offer less insurance options in an effort to remain profitable, or be driven out of the market. But driving insurers out of the market reduces competition, leaving motorists with less choice and less insurance options. In some cases, high-risk drivers may not even be able to find insurance.

Such a chain of events occurred under the NDP price controls. Auto insurance companies were forced to become unprofitable and thus attempted to minimize their losses by cancelling broker contracts and limiting non-mandatory coverage for Albertans. For every dollar they received in premiums, insurers ended up paying out as much as $1.30 in claims and costs, clearly an unsustainable situation. The same thing resulted from the UCP’s general rate “pause” in 2023, as well as its subsequent 2024 “safe driver” rate cap replacement.

In fact, a recent report by Statistics Canada found that approximately one-third of Alberta’s insurance companies were unprofitable in 2023, and several insurers had exited the market. The insurers that fled the market cited the unprofitable and challenging conditions created by the government, pointing specifically to the general “pause.”

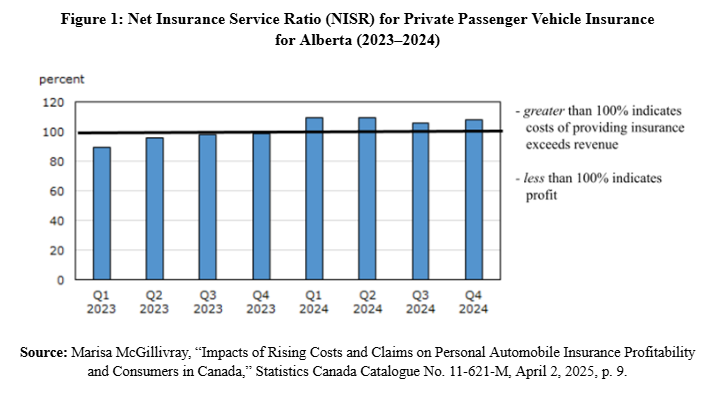

An insurer’s profitability is measured by the Net Insurance Service Ratio (NISR). The NISR measures a company’s profitability by comparing its expenses in providing insurance services against the revenue generated from the sale of those services (i.e., claims and expenses divided by premiums earned). The lower the NISR percentage, the greater the profitability; the higher the NISR percentage, the lower the profitability. In general, auto insurance is considered profitable when the NISR is below 80% to 85%.

Figure 1 illustrates the rapid decrease in profitability following the general pause of 2023. The industry’s NISR rose to 100% by the end of the third quarter and continued above 100% even after the general pause was replaced by the “safe driver” rate cap.

Despite clear evidence from their own experience, the current Government of Alberta continues to impose price controls, ignoring how rate caps distort pricing, destabilize the market, and inflict real harm on both insurers and Albertans.

Lessons from Europe: Competitive and Market-Driven Determination of Premiums

As mentioned above, when governments impose price controls in response to public pressure, insurers become unprofitable and leave the market. Once price controls are lifted though, the remaining insurers need to raise their premiums to recover costs and losses that accumulated when the price controls were in place. As premiums rise, public pressure on the government intensifies, prompting the government to implement yet another round of price controls. Every time this cycle repeats, more competition is driven out of the market and other insurance companies are dissuaded from entering the market.

The Alberta government needs to try something different. It should seriously consider following Europe’s example and allowing premiums to be determined solely by competition and market forces.

Price controls on auto insurance simply do not exist in the European Union (EU), nor do they exist in Switzerland. Overseas, public authorities focus on regulatory oversight and competition, rather than instituting rate caps and reviewing and approving rate increases. Some countries do legally define pricing-related mechanisms such as bonus–malus schemes, and certain specific segments may involve approved surcharges. However, under EU competition and insurance directives, premiums must be market-determined; insurers are free to price risk based on what they deem necessary. In Switzerland, the insurance model is market-oriented with no rate caps, and insurers are completely free to set their premiums based on the risks they are insuring.

Conclusion

If the current government continues to impose price controls, then both Albertans and their auto insurers can expect to continue to suffer the pernicious effects of those rate caps, never achieving sustainable premiums. The data clearly show that all the price controls that have been implemented have made the market unstable by keeping premiums artificially low and distorting the pricing of risk. As a result, they have damaged the industry’s profitability and reduced competition, threatening to gut the auto insurance market and leaving Albertans with few choices.

The government of Alberta must follow Europe’s example by letting competition drive the market through freely determined premiums and rate changes. The only way to sustain lower premiums, to have a stable auto insurance industry, and to provide Albertans with real choice is to remove all forms of rate caps and price controls once and for all.